In today's modern world, the aging experience is increasingly defined by extended lifespans that often outpace healthspans. As people live longer, the accumulation of health events shifts the burden of healthcare from episodic medical visits to sustained, complex support. Aging services in the United States, encompassing senior living communities, long-term services and supports, and home care, are approaching a period of structural stress. Demographic aging, rising clinical complexity, and widening affordability gaps are colliding with delivery models originally designed around real estate, hospitality, and episodic care. The result is growing misalignment between how senior care is organized and what older adults and their families increasingly require. In addition, there is the reality of capturing remaining private-pay dollars before those sources are depleted and Medicaid rates become the primary reimbursement.

For family members like Mark and Sarah, this structural mismatch becomes personal with little warning. Their 82-year-old mother, Helen, lives alone in Pennsylvania, more than four hundred miles away from either of them. When a late-night call reveals that she slipped in her bathroom and remained on the floor for two hours, a familiar sequence followed: urgent travel across state lines, improvised care arrangements, and reassurances that offer temporary stability but little for long-term safety and confidence. Helen's teacher's pension and modest savings place her squarely in what researchers describe as the "forgotten middle": too affluent to qualify for Medicaid, yet unable to afford private-pay senior living communities that increasingly dominate the market.

This pattern is no longer exceptional. Mark and Sarah's experience with their mother reflects the emerging American experience of aging. Families are navigating longer lifespans marked by higher clinical acuity, fragmented care delivery, and financial exposure that few anticipated or planned for. The number of middle-income older adults caught between Medicare or Medicaid eligibility and private-pay affordability is projected to reach nearly 16 million people by 2033 (NORC, 2022). While Medicare is a critical component, Medicare (Part A) currently covers only up to 100 days of skilled nursing care per benefit period; as a result, it is only a short-term bridge if a patient needs long-term coverage. The resulting strain is borne not only by seniors themselves but also by a vast informal caregiving workforce of spouses, adult children, and extended family, who absorb care coordination, logistical complexity, and emotional load with limited external support.

The question facing the aging services sector is not whether change is coming, but how it will unfold. Will aging services evolve through deliberate system-level redesign, or through reactive responses to crises in access, staffing, and solvency? The answer will determine not only which organizations endure, but whether aging becomes more predictable, dignifying, and humane, or it becomes increasingly precarious.

The Structural Realities Forcing Aging Services to Change

The aging services market is being reshaped by a set of converging forces that are altering demand, economics, governance, and operating expectations.

Demographic Growth Is Driving Higher Clinical Acuity

The United States is in the midst of the "Silver Tsunami." By the mid-2030s, adults aged 65 and older will outnumber children under 18 for the first time in American history. Growth is fastest among adults over 75, the cohort most likely to require ongoing medical and supportive services. While people are living longer, they are also spending more years managing multiple chronic conditions.

This dynamic has materially changed the operating reality of senior living and long-term care providers. Resident acuity has risen across settings even as reimbursement is rate-constrained, exposing the limits of models not designed for continuous clinical coordination or risk management.

The Affordability Crisis and the Forgotten Middle

Affordability represents the central economic challenge in aging services. Approximately three-quarters of American seniors cannot afford market-rate senior living on income alone. The forgotten middle includes individuals who exceed Medicaid eligibility thresholds but lack the assets required to cover private-pay costs, which often range from $5,000 to $8,000 per month.

Despite rapid growth in this population, much of the sector remains oriented toward higher-wealth segments, where margins are more predictable. Medicare further compounds the gap by covering acute episodes while excluding long-term custodial care. Serving the middle market requires balancing high service intensity, thin margins, and limited public subsidy, a challenge that prevailing business models have struggled to address at scale, despite sustained capital interest in private-pay, capital interest in private-pay segments.

Occupancy Recovery Obscures Financial Fragility

Occupancy across senior living communities has largely recovered from pandemic lows. The senior living occupancy reached roughly 90 percent by late 2025, while new supply fell to approximately 2.3 percent of inventory, the lowest level in more than a decade (Cushman & Wakefield, 2026). In skilled nursing facilities, the decline in usable beds is twice that of licensed beds, driven by staffing constraints.

On the surface, these indicators suggest stabilization. In reality, they obscure deeper financial stress. Labor costs account for the majority of operating expenses in aging services, and 37 percent of institutional investors cite workforce conditions as the single greatest risk to senior living valuations, ahead of interest rates, supply, or regulatory concerns (Cushman & Wakefield, 2026). Wage inflation, turnover, and reliance on agency staffing continue to compress margins even as occupancy improves. Occupancy alone is no longer a reliable indicator of organizational health.

Repositioning Has Replaced New Development

Rising construction costs and constrained debt markets have slowed new development and shifted growth strategies toward repositioning existing assets. Since 2020, construction costs have increased an estimated 30 to 40 percent.

Nearly 45 percent of senior housing properties are more than 25 years old (Senior Housing News, 2025), often built for an era before digital health, contemporary accessibility standards, or higher acuity care expectations. As a result, mergers, affiliations, selective acquisitions, and campus modernization have replaced greenfield development as the dominant growth pathways, accelerating consolidation and widening performance gaps.

Residents Are Demanding Greater Voice and Transparency

Resident expectations are rising alongside financial and operational pressure. Within entrance-fee continuing care retirement communities (CCRCs), in particular, residents increasingly see themselves as financial stakeholders rather than as passive recipients of care. Baby Boomers are more consumer-oriented and more inclined to demand transparency than prior generations.

These expectations extend beyond amenities to governance and capital allocation. While greater engagement can strengthen trust and community resilience, it also introduces governance complexity at a time when organizations must make difficult trade-offs under margin pressure.

Technology Is Separating Market Leaders from Laggards

Technology adoption is becoming a key differentiator. Leading organizations are investing in predictive analytics, interoperable electronic health records, telehealth, and remote monitoring to improve outcomes and stabilize operations. Others lag due to limited capital, technical expertise, or change management capacity.

As with capital, technology is acting as a force multiplier, widening performance and capability gaps rather than uniformly lifting standards across the sector.

The Case for Integrated Care

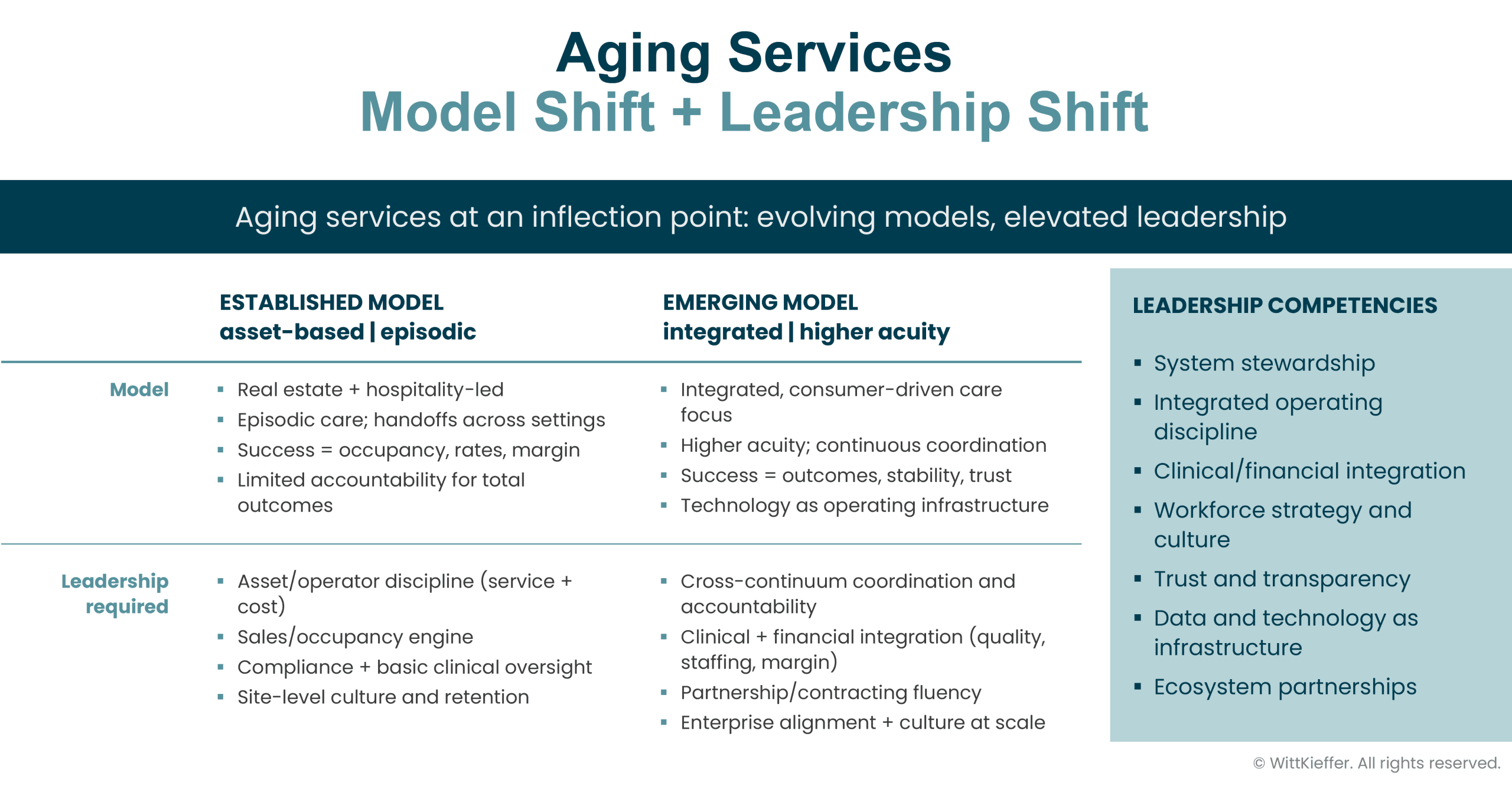

Fragmentation in aging services is structural rather than accidental. Housing, healthcare, and social supports are financed and regulated separately, leaving no single entity accountable for outcomes or the total cost of care. Integrated care models seek to reverse this logic by aligning clinical delivery, operations, and financial accountability.

The program of all-inclusive care for the elderly (PACE) represents the most fully integrated model. Operating under global capitation, PACE organizations are financially accountable for outcomes, making prevention economically rational. Hospitalization rates are meaningfully lower than those of comparable fee-for-service populations, and satisfaction with coordination is consistently high.

Capital has accelerated PACE growth. Following regulatory changes allowing for-profit participation, enrollment in for-profit PACE programs grew by 173 percent between 2016 and 2022, with more than half of for-profit programs backed by private equity or venture capital (NORC, 2025). Yet scale remains limited. As of 2026, fewer than 92,000 participants are served across 202 programs nationwide, reflecting regulatory, eligibility, and execution constraints (National PACE Association, 2026).

Institutional special needs plans (I‑SNPs) embedded within senior living communities offer a more accessible integration pathway. When well executed, they reduce hospital admissions by 20 to 35 percent by addressing clinical deterioration before it escalates into emergencies. Performance variability, however, reinforces a broader lesson: integration is not a contract or product, but an operating capability.

Leadership for an Integrated Future

The transition from fragmented to integrated care cannot be achieved through capital, contracting, or technology alone. It requires leadership capable of managing clinical, regulatory, labor, and financial complexity simultaneously.

As care models become more integrated and risk-bearing, tolerance for execution error declines. Across aging services platforms, investor outcomes increasingly diverge based not on subsector exposure, but on leadership depth and operating discipline once capital is deployed. Weaknesses that remain latent in asset-based models surface quickly in integrated environments.

Leadership, in this context, is shifting from operating discipline to system orchestration. The challenge is not optimizing a single asset or service line, but aligning clinical risk, capital deployment, and care delivery across a fragmented continuum.

The transformation of senior care requires a new type of leader, one who navigates complexity with both analytical precision and human understanding. While traditional skills like operational efficiency and financial acumen still matter, the future belongs to those who blend logic with empathy and strategy with compassion.

Strategic savvy and moral clarity. Integrated care models are intricate ecosystems relying on predictive analytics and multidisciplinary coordination. Leaders must logically grasp how clinical workflows interact with reimbursement mechanisms and how small operational inefficiencies can lead to large-scale failures. Clarity of thought is a prerequisite for growth in this domain.

Deep care for the community. Empathy must be paired with altruism, particularly when organizations face pressure to prioritize occupancy over resident well-being. A stewardship mindset, placing the resident first, is not just an ethical stance; it is a strategic advantage that generates long-term value and loyalty.

Resilience. Psychologist Angela Duckworth identifies grit, the combination of passion and perseverance, as a core element of success in challenging environments (Angela Duckworth, 2016). For senior care leaders, resilience means absorbing pressure without transmitting it downward and maintaining optimism in the face of systemic challenges. Purpose acts as a stabilizing force; those who see this work as a calling find the stamina to move beyond compliance toward excellence.

Meeting the Moment in Aging Services

Aging services have reached a point where incremental adjustments are no longer sufficient. The pressures reshaping the sector are structural and persistent. Integrated care demonstrates that a more stable, humane, and economically aligned approach is possible, but it is operationally unforgiving.

The implications of this shift extend beyond organizations and investors; they are felt most directly by families navigating an increasingly complex and fragmented system. For families like that of Mark and Sarah, the future of aging services will ultimately be measured not in abstract models or reimbursement structures, but in whether Helen's next moment of vulnerability is met with coordination, continuity, and care that feels both dependable and dignified.

The organizations that endure will be those that treat aging services not merely as assets to be managed, but as systems to be stewarded, supported by capital that absorbs volatility and leaders capable of translating complexity into coherent, sustained performance.

Sources

Angela Duckworth (2016). Grit: The Power of Passion and Perseverance. New York: Scribner