Private equity (PE) firms that invested in healthcare services platforms before 2020 entered with familiar playbooks: consolidate fragmented markets, optimize and systematize operations, capture synergies, and exit within 4 to 5 years at attractive multiples. Today, however, many of those same investors and their leadership teams face a starkly different reality: changing investor appetites, compressed valuations, elevated leadership turnover, and operational headwinds that stretch value-creation timelines well beyond initial underwriting. The confluence of macroeconomic pressure, intensified regulatory scrutiny of healthcare consolidation, state-level regulation, and sector-specific operating challenges creates a perfect storm.

The healthcare PE landscape reflects this storm. While US healthcare deal value grew 43% to $138.5 billion in 2025, deal volume grew a modest 2.6%. And, the healthcare services segment, once the leading segment within healthcare PE, was flat in 2025. Physician Practice Management (PPM) deal activity has been particularly hard hit. PPM deal count was down 18% in 2025, and Q4 2025 was the lowest quarter for deal activity since Q2 2020 — by a significant spread — and the second lowest quarter since at least 2017 (PitchBook, 2026).

However, not all PPM subsegments face equal headwinds. PPM exit count increased 57.1% in 2025, which may be viewed as a potential early indication of improved deal activity in 2026. Subsegments expected to remain strong in 2026 include oncology (up 66.7% year-over-year in 2025) and musculoskeletal (up 33.3%) (PitchBook, 2026). This divergence underscores that while the overall PPM market faces pressure, platforms in resilient subsegments with strong fundamentals and operational excellence can still achieve successful exits.

The storm confronting healthcare PE results in extended hold periods, which now routinely stretch to seven years or more: 29% of current US PE-backed healthcare assets are aged 7+ years, while another 37% are aged 4 to 6 years (PitchBook, 2026). As of late 2025, 37.1% of PE deals from the 2017 cohort remained held by their PE firms, a percentage significantly higher than the 26.4% of the 2012 cohort that remained after the same duration (PitchBook, 2025). With an estimated PE-held healthcare services company inventory of 933 (1,526 across all PE-held healthcare companies), there is an 11.4-year backlog based on the four-year trailing average of annual exits.

The PE healthcare inventory problem is real and growing. Assets that matured during a market downturn have been harder to exit, with the delay in monetization adding further to PE inventory. The issue is exacerbated by the group of PE-backed assets approaching maturity in the coming years. PE-backed assets from 2021, which was a record dealmaking year, have been exiting at an even slower pace than the 2017 cohort (PitchBook, 2025).

In healthcare services specifically, aged inventory is concentrated in several subsectors: dental, mental health, home-based care, musculoskeletal, clinical staffing, dermatology, and vision. Collectively, these seven subsegments represent over 400 companies with holding periods of at least five years (PitchBook, 2026). These stranded assets, often held at above-market valuations, are limiting the pace of capital redeployment and forcing sponsors to focus on organic operational value creation rather than financial and integration engineering.

For operators on the ground, the implications are profound. Healthcare organizations are contending with C-suite turnover, persistent workforce shortages, clinician burnout, payer friction in revenue cycle management (RCM), and data fragmentation inherited from aggressive roll-up strategies. These pressures suppress run-rate EBITDA, delay efficiency capture, and push liquidity events further into the future.

This article explores the growing strain on PE‑backed healthcare platforms derived from extended hold periods and operational complexity. It highlights the leadership pressure points that determine whether value creation stalls or gains momentum and offers a practical playbook to help investors and leadership teams navigate long holds and strengthen performance through uncertain exit environments.

Impactful Leadership Matters More Than Ever

The shift in the PE landscape is dramatic, particularly in healthcare services. This reality, combined with valuation compression and regulatory scrutiny, creates a new imperative: value creation now depends squarely on organic growth, disciplined capital deployment, and operational excellence.

For many leadership teams, this is a different game entirely. Leaders who joined expecting a 4- to 5-year sprint to exit now face a marathon, often without updated compensation structures or the strategic and operational recalibration needed to sustain performance over extended horizons. As a result, executives will evaluate their personal value creation plans — and the disruption those might have experienced — as rigorously as their companies' plans.

Our work with PE-backed healthcare platforms reveals critical pressure points where impactful leadership makes the difference between value creation and value erosion.

Leadership Continuity as Competitive Advantage

Elevated C-suite turnover is one of the most disruptive forces in PE-backed healthcare organizations. Our research on PE-backed healthcare CFOs reveals that many platforms experience CFO transitions within two years post-acquisition (WittKieffer, 2025-I), often driven by misalignment on strategy, burnout from relentless value-creation pressure, or attractive external opportunities. CFO churn is especially damaging because it disrupts financial planning and analysis (FP&A) transformation, revenue cycle optimization, and the financial narrative required for exit readiness.

Stabilize the Keystone Role of a CFO

The CFO role is the keystone of value creation in PE-backed healthcare platforms. CFO turnover correlates directly with plan resets, delayed execution, and lost institutional knowledge.

The CFO profile for extended holds must blend operational rigor with strategic communication. The best candidates bring deep expertise in RCM, cash flow optimization, FP&A, and systems integration, while also excelling at stakeholder communication, value-creation narrative development, and cross-functional leadership.

Practical moves to stabilize the CFO role include:

- Retention packages: Lock in CFOs with milestone-based equity refreshes tied to operational achievements and exit readiness.

- Transformation roadmaps: Define clear 18- and 36-month finance transformation goals (close speed, KPI unification, cash conversion improvement) that provide purpose and measurable progress.

- Succession planning: Formalize step-in plans for interim coverage and develop internal finance talent pipelines to reduce external dependency.

The challenge extends beyond individual roles. Organizations experiencing C-suite churn face compounding challenges: loss of institutional knowledge, stalled strategic initiatives, and erosion of investor confidence — all of which delay performance gains and extend hold periods further.

Leadership action: Proactively assess leadership team alignment, capabilities, and retention risk before transitions become crises. Deploy targeted retention strategies, refresh equity structures for extended holds, and build succession bench depth. Engage external leadership advisors early to understand the talent market and benchmark current leaders against best-in-class capabilities.

Clinical-Financial Alignment as Growth Engine

The tension between PE expectations for rapid EBITDA growth and clinical imperatives for quality and safety is operational, not just philosophical. When clinical leaders feel marginalized or quality metrics are decoupled from executive incentives, the result is predictable: clinician burnout, turnover, declining patient satisfaction, and, ultimately, weaker financial performance.

This misalignment is particularly acute in PPM platforms, where deal activity declines were led by weakness in gastroenterology (down 85.7%), fertility (down 50%), ear, nose, and throat (down 38.9%), and dental (down 36.5%) (PitchBook, 2026). According to Joel Rush, partner at McDermott Will & Schulte LLP, the PPM industry is "still working through the COVID-valuation and productivity bubble and that era of exceptionally high valuations for add-on acquisitions, given leverage involved and operational challenges. Layer on top of that state-level regulatory activity with a keen interest in PE ownership and the corporate practice of medicine."

Leadership action: Integrate clinical quality metrics into executive performance scorecards. Ensure clinical leaders have a genuine voice in enterprise decisions. Build compensation structures that reward sustainable growth, not just short-term margin expansion. Use team coaching to unify leadership perspectives and bridge gaps between clinical and financial priorities through facilitated dialogue and shared goal setting.

Revenue Cycle Excellence as Cash Flow Stabilizer

RCM remains a top operational stressor, with prior authorization delays, claim denials, staffing shortages in billing and coding, and payer contract complexity identified as the most significant challenges facing healthcare finance leaders. Many PE healthcare executives are prioritizing automation (robotic process automation for claims follow-up, AI-driven coding assistance) and outsourced managed services to stabilize net collections and reduce receivables days outstanding. However, implementation requires upfront capital and multi-quarter timelines — resources that are often constrained in high-leverage environments.

Leadership action: Appoint leaders with demonstrated revenue cycle transformation experience who can prioritize investments that deliver near-term and sustainable cash impact. Deploy interim leadership or on-demand project expertise to accelerate implementation and alleviate shortages in capacity or capability on the existing team. Establish clear KPIs that link RCM performance to leadership accountability and create timelines for remediation when early warning signs are triggered.

Data Integration as Decision-Making Foundation

Aggressive roll-up strategies frequently leave platforms with fragmented electronic health record systems, inconsistent data definitions, and no single source of truth. Without unified enterprise data, leadership teams cannot identify improvement opportunities, optimize integration and synergy capture, enhance clinical outcomes, or build credible exit narratives. This data fragmentation delays decision-making, obscures true performance, and ultimately prevents portfolio companies from capturing the full value of their consolidation efforts.

Leadership action: Appoint leaders who can drive technology and data adoption as an enterprise-wide priority, not just an IT project. Ensure the leadership team has the expertise to define data quality standards, implement integrated infrastructure that enables real-time performance visibility, and translate data insights into actionable business decisions.

The Leadership Playbook: A Structured Approach to Value Creation

In any context, investors and portfolio companies need a leadership playbook as robust as their operational and financial playbooks — one that directly unites value creation objectives with the critical leadership capabilities required to deliver results.

As we outlined in our previous report (WittKieffer, 2025-II), this playbook approach addresses three fundamental leadership needs across all phases of the investment lifecycle:

Emerging Opportunities in AI

At the 2026 J.P. Morgan Healthcare Conference, hospital systems spoke of renewed interest in PPM acquisitions, driven by the belief that the implementation of AI capabilities in the PPM setting will materially enhance efficiency and return profiles of these practices going forward, thereby enhancing long-term valuation prospects.

PPM organizations and multispecialty clinics and networks are well-positioned to benefit from the utilization of AI capabilities in their practices, beginning with ambient AI scribing technologies. Benefits include reduced documentation time and decreased administrative burdens on the entire staff, resulting in lower clinical cost of care as saved time allows for more patient visits. Additionally, automation will lower administrative headcount and create higher margins.

- Do you have the right people to define and lead the value creation plan?

- Are leaders aligned on strategic priorities, roles, and performance expectations?

- Can the team execute with the speed, agility, and cohesion required in this new context?

Ensuring that the right executives and teams are in place to drive performance presents a multi-layered challenge. It requires an understanding of how strategic objectives translate into business and talent needs, how leaders are assessed against those specific needs, and how to find or develop leaders who can perform across an inevitably dynamic investment period.

The Playbook Process

Individual assessment: Evaluate each leader's capabilities against the specific demands of the value creation strategy. This goes beyond resume review to include in-depth interviews analyzing leadership styles, communication preferences, technical expertise, and cultural fit. The goal is to identify gaps between current capabilities and future requirements before they become performance obstacles.

Team assessment: Ensure tight coordination between clinical, commercial, and operational leaders as misalignment can be debilitating to performance and patient safety. Team assessment promotes open dialogue, improves communication, and aligns leadership with strategic objectives. Facilitated team sessions help leadership teams identify pain points, build trust, and establish a unified vision to drive operational excellence.

Performance monitoring: Establish ongoing mechanisms to monitor leadership performance, not just financial or operational performance, along with offering constructive support for development. This includes regular check-ins on leadership effectiveness, team dynamics, and alignment with evolving strategic priorities.

However, as described earlier, the context for PE-held healthcare companies has fundamentally changed. When this happens, prior playbooks and performance expectations need to be revisited and reset, and executive teams realigned to the new playbook.

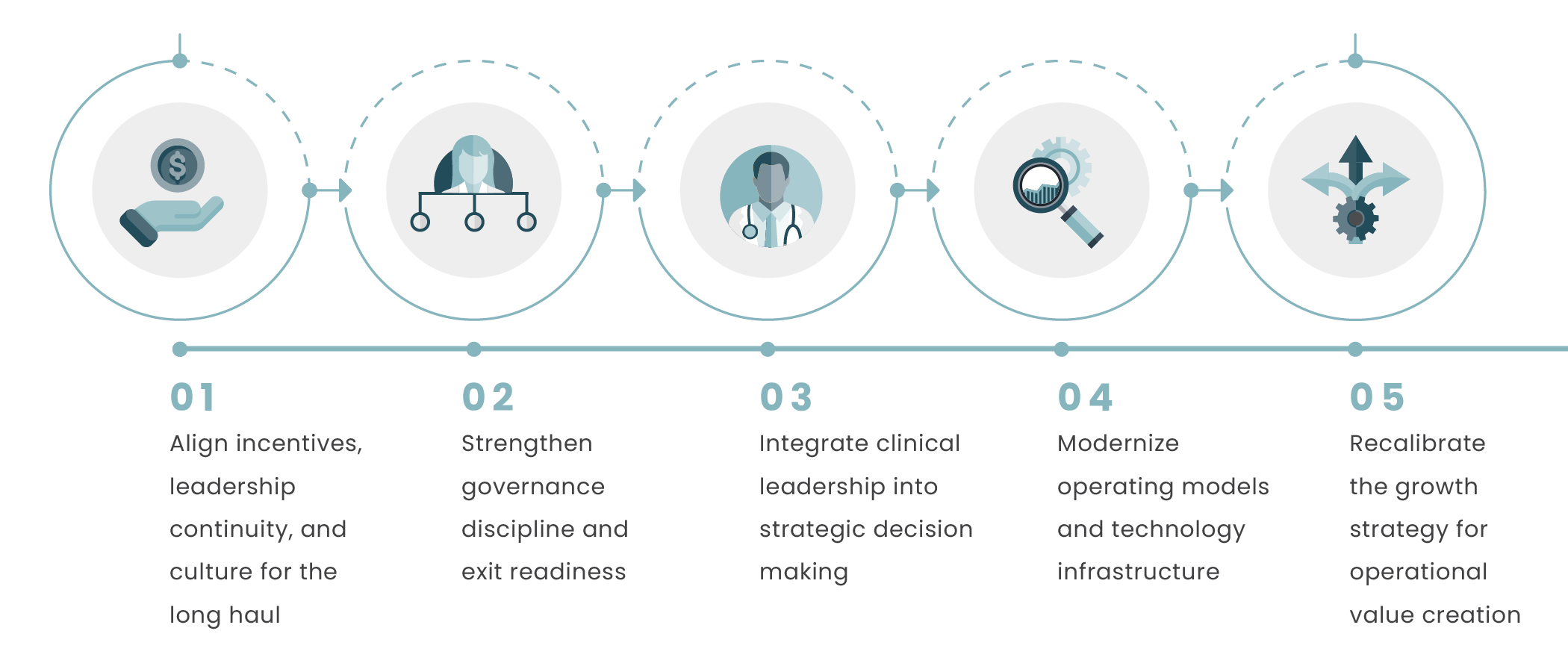

Five Leadership Imperatives: A Roadmap for the Long Hold

To navigate extended holds successfully, investors and leadership teams should focus on five leadership imperatives that address the most critical drivers of value creation and exit readiness.

Leadership Imperatives for Extended Holds

1. Align incentives, leadership continuity, and culture for the long haul

Management equity plans designed for a 2023 exit are misaligned when the actual exit is now projected for 2027 or beyond. Sponsors and boards must proactively reset equity and cash incentives: re-strike underwater equity incentives, introduce layered earn-outs tied to operational milestones, and refresh performance equity grants. Critically, incentive milestones should emphasize operational value creation, such as EBITDA growth, margin expansion, cash conversion, and quality metrics — rather than relying exclusively on exit value hurdles, e.g., multiple on invested capital (MOIC), set in an entirely different valuation context.

Securing leadership continuity requires more than compensation resets. Organizations should establish formal succession planning and talent maps, design retention packages competitive with external market pull, and maintain leadership scorecards for mission-critical roles. Practical moves include milestone-based equity refreshes tied to 18- and 36-month transformation roadmaps, formalized step-in plans for interim coverage, and regular talent reviews that identify flight risk before it becomes a crisis.

Culture and engagement are equally critical in extended holds. Leaders must reinforce organizational purpose, communicate transparently about timelines and strategy, and create forums for feedback and engagement. Regular town halls, updated strategic narratives, and visible leadership presence counter the fatigue and disengagement that threaten performance when the finish line keeps moving. Organizations that maintain momentum through transparent communication and purpose-driven leadership are better positioned to sustain performance and attract top talent even as hold periods extend.

2. Strengthen governance discipline and exit readiness

Longer holds demand more disciplined governance structures. Clarifying decision rights, meeting cadence, and escalation paths protects against quarter-to-quarter strategy whiplash and ensures consistent execution against long-term value creation plans. Leadership teams perform best when they understand realistic hold scenarios, potential continuation-vehicle structures, and interim liquidity pathways.

Sponsors should regularly communicate updated exit modeling and explore partial liquidity mechanisms — e.g., dividend recaps, minority stake sales, or GP-led secondaries — to maintain leader engagement and reduce uncertainty. Additionally, boards should establish clear exit readiness milestones: financial reporting quality, data room preparation, quality of earnings (QoE) readiness, and strategic narrative development. These governance disciplines ensure that when exit windows open, platforms can move quickly and command premium valuations.

3. Integrate clinical leadership into strategic decision-making

Embedding clinical leaders like chief medical officers and chief nursing officers in portfolio governance, aligning clinical quality metrics with executive incentive plans, and strengthening clinician voice in capital allocation decisions can bridge the gap between financial targets and clinical realities. This integration improves decision quality, enhances clinician engagement, and reduces the risk of quality or compliance failures that can derail exit readiness.

3. Recalibrate the growth strategy for operational value creation

Many platforms have paused M&A and must now optimize the assets already acquired. This requires hard decisions on centralization vs. local autonomy, rationalization of duplicative functions, and a technology enablement roadmap that unlocks near- and long-term productivity. Successful PPM platforms demonstrate that clarity on decision rights (particularly defining "the role of the center"), shared services design, and technology architecture are foundational to capturing consolidation synergies and improving both clinician experience and practice economics (Bain & Company, 2026).

Portfolio companies that invest early in data infrastructure, automation, and analytics are better positioned to demonstrate performance improvement and command premium valuations. Targeted automation in RCM, clinical documentation, and prior authorization can show accelerated ROI and free up capacity for higher-value work.

5. Recalibrate the growth strategy for operational value creation

For long-held platforms, the path to exit readiness requires shifting from acquisition-driven growth to organic expansion and operational optimization. Leadership teams should focus on five growth levers that demonstrate sustainable value creation to potential buyers.

Identify adjacencies that leverage existing relationships. Platforms with established patient, health system, or payer relationships can expand service offerings without significant customer acquisition costs. Examples include adding ancillary services (e.g., imaging, lab, infusion), expanding into complementary specialties, or offering value-based care coordination services that deepen existing partnerships.

Introduce direct-to-consumer models where appropriate. Reducing dependence on traditional reimbursement by developing private-pay or subscription-based service lines, such as integrative and functional medicine, direct primary care, women's health services, or AI-powered diagnostics, can improve margins and demonstrate revenue diversification to buyers. Self-pay pathways serve as a strategic bridge between innovation and reimbursement, allowing platforms to accelerate market entry for new services while building clinical evidence. However, success requires leadership with commercial expertise in consumer marketing, pricing strategy, and technology-enabled patient engagement — capabilities that differ fundamentally from traditional healthcare operations (WittKieffer, 2025-III).

Expand geographic presence in underserved markets. Rather than competing in saturated metro markets, platforms can achieve growth by entering underserved geographies where competition is lower, clinician recruitment is easier, and payer relationships can be established on more favorable terms.

Deploy digital engagement and telehealth strategies. Technology-enabled care delivery expands geographic reach without proportional cost increases, improves patient access and satisfaction, and demonstrates innovation that appeals to both strategic and financial buyers. Platforms that successfully integrate telehealth into care pathways show improved retention and higher revenue per patient.

These strategies shift the growth narrative from "we acquired so many practices" to "we built sustainable organic growth engines" — a story that commands premium valuations and appeals to strategic buyers seeking operational excellence, not just scale.

A Longer March, A Sharper Playbook

The era of quick flips and multiple expansions in healthcare PE has given way to a more demanding environment: one defined by elongated holds, compressed valuations, operational complexity, and leadership volatility. The data is clear: 37.1% of 2017 vintage deals remain unrealized (PitchBook, 2025), aged inventory spans multiple healthcare subsectors, and regulatory uncertainty continues to slow transaction activity.

PPM exit count increased 57.1% in 2025, rising from 21 to 33 exits — modestly above the nine-year average of 29 but representing early signs of improved liquidity (PitchBook, 2026). While exit volumes remain constrained, the uptick suggests sponsors are beginning to clear older assets, and subsectors like oncology and musculoskeletal show resilience that may support broader exit activity in 2026. Strategic buyers, particularly hospital systems, are expressing renewed interest in PPM acquisitions, driven by AI-enabled efficiency gains that promise to transform practice economics.

Outperformance in this environment will come not from financial engineering, but from disciplined incentive alignment, resilient organizational culture, leadership continuity, and visible operating traction in RCM, data infrastructure, and clinical quality. The playbook must change, but the opportunity for value creation remains.

Investors and leadership teams must move quickly to systematically assess leadership capabilities against the new context for value creation and take decisive actions to close gaps through targeted recruitment, development, or transition. Those that do will re-accelerate time to value, improve probability of success, and increase magnitude of returns.